Companies with strong business credit profiles can secure up to 30% more financing than those without credit history. This highlights how business credit can be a game-changer when securing favorable loan terms and funding for expansion.

For incorporated businesses, the stakes are even higher as creditworthiness impacts their ability to secure loans, lease equipment, or expand operations. Whether running a startup or a well-established LLC, understanding how to establish and leverage business credit is key to financial success.

What Is Business Credit?

Business credit measures a company’s ability to borrow money, purchase products or services, and establish trade lines based on its financial reputation, independent of its owners’ credit profiles. Credit agencies like Dun & Bradstreet, Experian, and Equifax assess it, assigning scores based on payment history, debt levels, and business longevity.

Key Differences Between Personal and Business Credit

Here are some significant differences between both Credits:

| Aspect | Personal Credit | Business Credit |

| Identifier | Linked to Social Security Number (SSN). | Linked to Employer Identification Number (EIN). |

| Scope | Evaluate individual creditworthiness. | Evaluates the financial health of a business. |

| Impact | Affects personal financial assets and liabilities. | Separates personal assets from business risks. |

| Credit Limits | Typically, lower credit limits. | Higher credit limits are designed for business needs. |

| Credit Agencies | Managed by Experian, Equifax, and TransUnion. | Managed by Dun & Bradstreet, Experian, and Equifax. |

Why Business Credit Matters

Following are some key reasons why business credit is essential for your Business success:

- Access Larger Credit Limits: Lenders typically offer higher credit amounts to businesses with firm credit profiles.

- Secure Favorable Terms: Businesses with good credit scores can negotiate lower interest rates, reducing overall costs.

- Protect Personal Assets: By establishing business credit, you can avoid using personal credit for company expenses, minimizing personal financial risk.

- Enhance Market Credibility: A strong credit score builds trust with suppliers, partners, and clients, showcasing your business’s reliability.

How Business Credit Impacts Growth

Business credit is pivotal in a company’s ability to expand and thrive. It provides access to critical funding, enabling businesses to invest in new equipment, open additional locations, or scale operations. Strong credit facilitates growth and empowers companies to seize opportunities that require immediate capital without straining personal finances.

Businesses with solid credit scores also often qualify for government contracts and vendor agreements. These arrangements are valuable for enhancing credibility and unlocking opportunities unavailable to companies with weak or nonexistent credit histories. With robust credit, businesses can negotiate better terms and pricing, giving them a competitive edge.

Building and maintaining strong business credit is not just about immediate benefits; it’s a long-term asset. Companies with good credit profiles are better positioned to weather economic downturns and sustain operations during challenging times. Businesses can ensure resilience, maintain financial independence, and protect their owners from unnecessary personal liability by focusing on strategic credit-building.

Consider Reading This: When Are Business Taxes Due 2024?

Can Incorporations Receive Business Credit?

Yes, incorporations, including LLCs and corporations, can receive business credit. Incorporating separates your personal and business liabilities, making establishing credit for your business easier.

Common Misconceptions

- Incorporation guarantees credit:

While incorporation is a step, creditworthiness depends on proper financial management and compliance.

- You need years of operation:

By following a set of guidelines, new firms can establish credit immediately.

Incorporation acts as the foundation, but proactive efforts like maintaining transparency and timely payments build creditworthiness.

How Do I Apply for Business Credit?

Applying for company credit involves thorough preparation and collaboration. Here’s a comprehensive step-by-step guide to help you set up a solid foundation for building your business credit profile:

Step 1. Open a Dedicated Business Bank Account

Separating your personal and business finances is essential to create clear and organized financial records. A dedicated business bank account shows lenders you’re serious about maintaining economic stability. Use this account solely for business-related activities, including receiving payments and paying expenses. This practice keeps your financial records tidy and demonstrates to lenders that your business is managed professionally.

Here, you can learn more about how to open a business account.

Step 2. Ensure Your Business Is Properly Registered

Proper business registration establishes its legal identity and is essential for building business credit. You must file Articles of Incorporation (or equivalent documents) with your state and choose the appropriate business structure (e.g., LLC, corporation). This step provides your business with legal protection and credibility. Additionally, obtaining an Employer Identification Number (EIN) from the IRS is crucial for identifying your business during financial transactions.

Step 3. Establish a Relationship with Credit Reporting Agencies

Building relationships with credit reporting agencies is crucial in establishing your business’s credit profile. Start by applying for a DUNS Number with Dun & Bradstreet, a standard identifier that helps you build your business credit history. Additionally, monitor your business credit reports regularly to catch and resolve any inaccuracies that might impact your score.

These steps will set your business up for successful credit building, providing the credibility needed to secure funding and partnerships. Keeping your financial records organized and staying proactive with credit agencies will help pave the way for a strong credit profile, boosting your business’s growth and stability.

Consider Reading This: How to Get a Startup Business Loan With No Money?

Five Easy Steps to Establishing Business Credit

Before establishing a good credit score, defining what a credit score is is essential.

Understanding Business Credit Scores

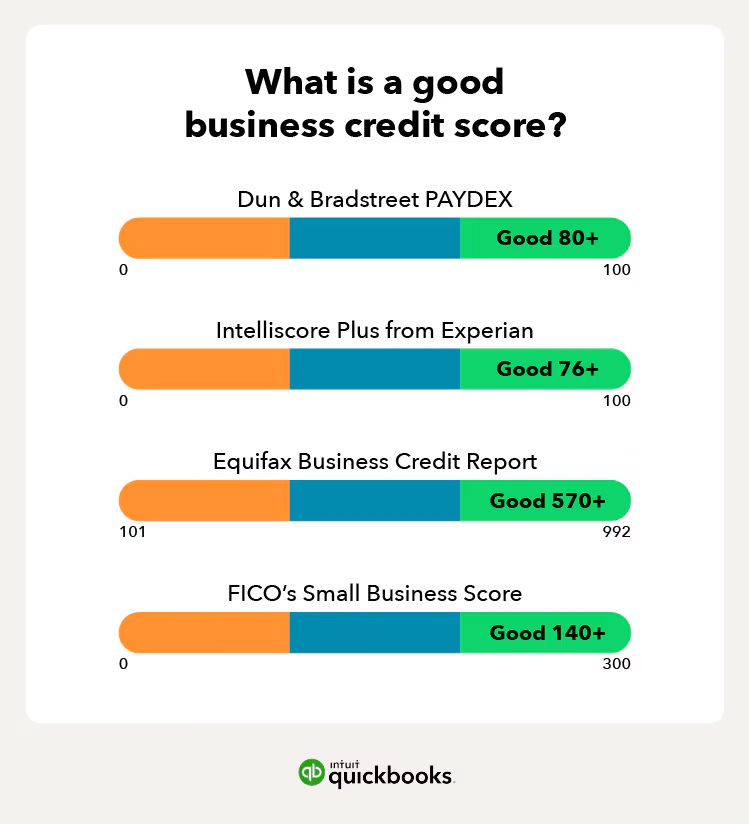

A business credit score is a numerical representation of your company’s creditworthiness, used by lenders, suppliers, and potential partners to gauge your financial health. It differs from personal credit scores, which are tied to individuals. Business credit scores typically range from 0 to 100, with higher scores indicating more robust credit profiles.

Building and maintaining good business credit requires proactive management and consistent practices. Here’s how to keep your credit profile strong and establish a lasting foundation for your business:

Step 1. Maintain On-Time Payments

Timely payment of all bills, loans, and credit obligations is crucial for maintaining a good credit score. Ensure you pay your suppliers, service providers, and other vendors who report to credit bureaus on time. This consistent behavior signals financial responsibility and builds trust with lenders and credit agencies.

Step 2. Monitor Your Business Credit Reports Regularly

Regularly checking your business credit reports can help you catch inaccuracies or fraud early. Each major credit bureaus, Dun & Bradstreet, Experian, and Equifax, offers business credit monitoring services. Staying proactive about your credit profile allows you to address issues before they impact your creditworthiness.

Step 3. Keep Debt Levels Manageable

Managing your debt load and ensuring it doesn’t exceed your revenue is essential for long-term financial stability. High debt-to-income ratios can negatively impact your credit score and make future financing difficult. To keep your credit healthy, try to maintain a debt level that your business can easily handle, paying down outstanding debts as soon as possible.

Step 4. Build Relationships with Lenders and Credit Bureaus

Cultivating relationships with financial institutions and credit bureaus can be advantageous. Open communication with these entities helps you understand how they assess your credit and allows for a smoother process when applying for financing. Strong relationships can also help you secure better rates and terms as your credit profile improves.

Step 5. Ensure Compliance with Legal and Financial Standards

Make sure your company complies with all legal and regulatory requirements. This includes timely filing annual reports, meeting tax obligations, and holding necessary business meetings. Compliance supports your legal standing and reinforces your business’s perception as reliable and stable.

For more simple establishment, Follow this:

Long-Term Strategies for Establishing Business Credit

Building business credit doesn’t stop at opening an account and getting a DUNS number; it involves ongoing practices that strengthen and sustain your credit profile.

- Diversify Your Credit Mix: Apply for different types of credit lines (e.g., business credit cards, lines of credit, loans) to show a balanced credit profile. A diversified mix demonstrates your ability to manage various financial products, which can help improve your score.

- Leverage Trade Credit: Partner with vendors and suppliers who offer trade credit and ensure that they report payment data to credit bureaus. Maintaining positive payment patterns can further enhance your credit history.

- Focus on Long-Term Financial Planning: Keep your business growing with a well-outlined financial strategy. Planning includes setting budgets, creating financial projections, and maintaining an emergency fund to mitigate unexpected financial disruptions.

By implementing these strategies and maintaining diligent financial practices, your business can achieve and sustain a strong credit profile, opening doors for better funding opportunities and a more secure financial future.

Benefits of Incorporations for Business Credit

Limited Liability Protection

One of the primary advantages of incorporating your business is the protection it offers to your assets. Your assets, such as your home and savings, are generally protected from financial difficulties or debts. This separation provides peace of mind and encourages entrepreneurs to pursue growth without fearing personal financial ruin.

Credibility with Lenders

You are incorporating signals to lenders and financial institutions that your business is professional and severe. This level of credibility can play a significant role in securing financing, as lenders are more inclined to trust companies that operate as legal entities over those that run as sole proprietorships. This trust can translate to faster loan approvals and better interest rates.

Access to Capital

Corporations and LLCs often have more access to significant capital than sole proprietorships. They can issue stock, attract investors, and access higher credit limits, enabling them to secure larger loans and more favorable terms. This is a crucial advantage for companies looking to scale their operations or fund significant business initiatives.

Growth Opportunities

Beyond financial benefits, incorporation positions your business for long-term growth. It provides a structured framework that helps companies operate smoothly, manage assets, and respond to market opportunities flexibly. The ability to offer shares to investors can also provide a financial influx that fuels innovation and expansion.

Consider Reading This: Top 10 Business AI Tools By ABC Media Net

Challenges in Receiving Business Credit As an Incorporation

Despite the benefits, there are some challenges you may also face while applying for and establishing a business credit as an incorporation. Here are some of the most common and essential to consider:

Ongoing Compliance

Maintaining compliance with federal, state, and local regulations requires time and organization. This includes submitting annual reports and tax filings and paying applicable state fees. While these are manageable, they need attention to detail and consistent effort.

Potential Personal Liability

Although incorporation protects personal assets, poor management or misconduct can lead to personal liability. Failing to separate personal and business finances or engaging in unethical practices can expose you to risk. Following corporate formalities is vital to mitigate this.

Cost of Incorporation

Initial and ongoing costs, such as legal and registration fees, can add up. Maintaining incorporation status, including annual fees and compliance costs, for smaller businesses can be financially burdensome.

Administrative Burden

Operating an incorporated business involves more paperwork and management than a sole proprietorship. This includes holding meetings, maintaining records, and ensuring compliance, which can take time and resources.

By understanding the benefits and challenges associated with incorporation, businesses can make informed decisions that align with their growth strategies and long-term objectives. It’s essential to weigh these factors carefully and consider professional guidance to navigate the complexities of incorporation effectively.

Tips for Strengthening Business Credit

Leverage Financial Services

One way to protect your business credit is by using business insurance. Insurance helps mitigate financial risks, ensuring your company can handle unexpected expenses without impacting your credit score. Types of insurance include general liability insurance, property insurance, and professional liability coverage. For more details on selecting the right insurance policies for your business, visit source on insurance basics.

Consult Professionals

Seeking advice from financial experts can provide a significant advantage when structuring loans and credit terms. Professional financial advisors can help you choose the best lending products and understand terms that align with your business’s economic health. Consulting with experienced financial planners or accountants ensures that your business strategy is on the right track for long-term credit management.

Monitor Credit Reports

Regularly reviewing your business credit report helps you catch any inaccuracies or fraudulent activities that could negatively impact your score. Address any discrepancies as soon as you spot them to maintain a positive credit history. Services like Dun & Bradstreet, Experian, and Equifax can provide comprehensive credit reports. Stay proactive to ensure your credit remains in good standing.

Conclusion

Establishing and maintaining strong business credit is crucial for any incorporation aiming for growth, stability, and financial resilienceBusinesses can enjoy numerous advantages by understanding what business credit is, how it differs from personal credit, and following a strategic approach to applying for and maintaining it. Incorporation offers limited liability protection, credibility with lenders, and better access to funding. However, it also comes with ongoing compliance responsibilities, costs, and the need for careful management.

Want More Personalized Financial Advice:

Frequently Asked Questions (FAQs)

What is considered business credit?

Business credit refers to a company’s ability to obtain financial products and services based on its creditworthiness. This is separate from personal credit and is linked to your business’s Employer Identification Number (EIN). Credit bureaus assess business credit, impacting your access to loans, credit cards, and supplier relationships.

What’s the difference between business credit and corporate credit?

While “business credit” is a general term for any type of business financing or creditworthiness, “corporate credit” specifically refers to the credit profile of a corporation. Business credit bureaus assess both, but corporate credit may be seen as more established due to the company’s legal structure and financial backing.

Do businesses have their credit?

Yes, businesses have credit scores separate from the owner’s credit. This business credit score is based on the business’s financial health and is assessed by credit reporting agencies such as Dun & Bradstreet, Experian, and Equifax.

Who pulls business credit?

Lenders, suppliers, and other financial institutions often pull business credit reports to evaluate a company’s creditworthiness before extending loans, credit lines, or trade credit. Business credit reports assess financial stability, payment history, and reliability.

What’s the difference between personal and business credit?

Personal credit is tied to an individual’s Social Security Number (SSN) and reflects financial behavior. On the other hand, business credit is tied to the company’s EIN and evaluates the business’s economic health. While personal credit affects individual borrowing, business credit determines a company’s ability to secure financing and partnerships.

What is a corporate credit?

Corporate credit is the credit profile specifically associated with a corporation as opposed to other business structures like LLCs or sole proprietorships. It can secure funding under the corporation’s name, independent of the owner’s credit.

How do I establish business credit for my LLC?

To establish business credit for an LLC, register your business correctly, apply for an EIN, open a dedicated business bank account, and apply for a DUNS number. You should also ensure compliance with local, state, and federal regulations and establish vendor relationships that report to credit bureaus.

How to get business credit for a startup?

Getting business credit for a startup involves creating a business profile, setting up a business bank account, and building a credit history through small credit transactions and timely payments. Establishing relationships with suppliers and vendors that report to credit agencies can also help build credit over time.

What is a business credit file?

A business credit file is a record maintained by credit bureaus that documents a company’s credit history, including payment behavior, outstanding debts, and credit applications. This file highlights a business credit score that lenders use to determine creditworthiness.

Do you receive business credit as an incorporation?

Yes, incorporated businesses can receive business credit. Still, eligibility depends on meeting specific requirements, such as having a registered business name, an EIN, and a business credit profile with reporting agencies like Dun & Bradstreet. Incorporating a business can also enhance its credibility with lenders and improve access to more significant credit limits and better loan terms.