According to a 2023 survey by the National Endowment for Financial Education, 70% of grown-ups feel stressed about money matters at some point in their lives.

Managing finances can feel overwhelming, but what if there were a way to simplify the process? Enter the personal finance flowchart, a visual tool designed to break down complex financial decisions into easy-to-follow steps. Think of it as a roadmap to financial stability and growth. This guide will not only explain the concept of a personal financeflowchart but also equip you with the knowledge to create one tailored to your unique needs.

What’s a Personal Finance Flowchart?

A personal finance flowchart is a visual representation of your financial journey. It organizes key financial activities, such as budgeting, saving, and investing, into a logical sequence, making it easier to track progress and make informed decisions. For example, a flowchart might guide you to first establish an emergency fund before moving on to paying off high-interest debt or investing in retirement accounts.

By visualizing your financial goals and the steps required to achieve them, a flowchart helps clarify personal finance and empowers you to take control of your money.

Steps to Create a Personal Finance Flowchart

Creating a personal finance flowchart involves following these essential steps:

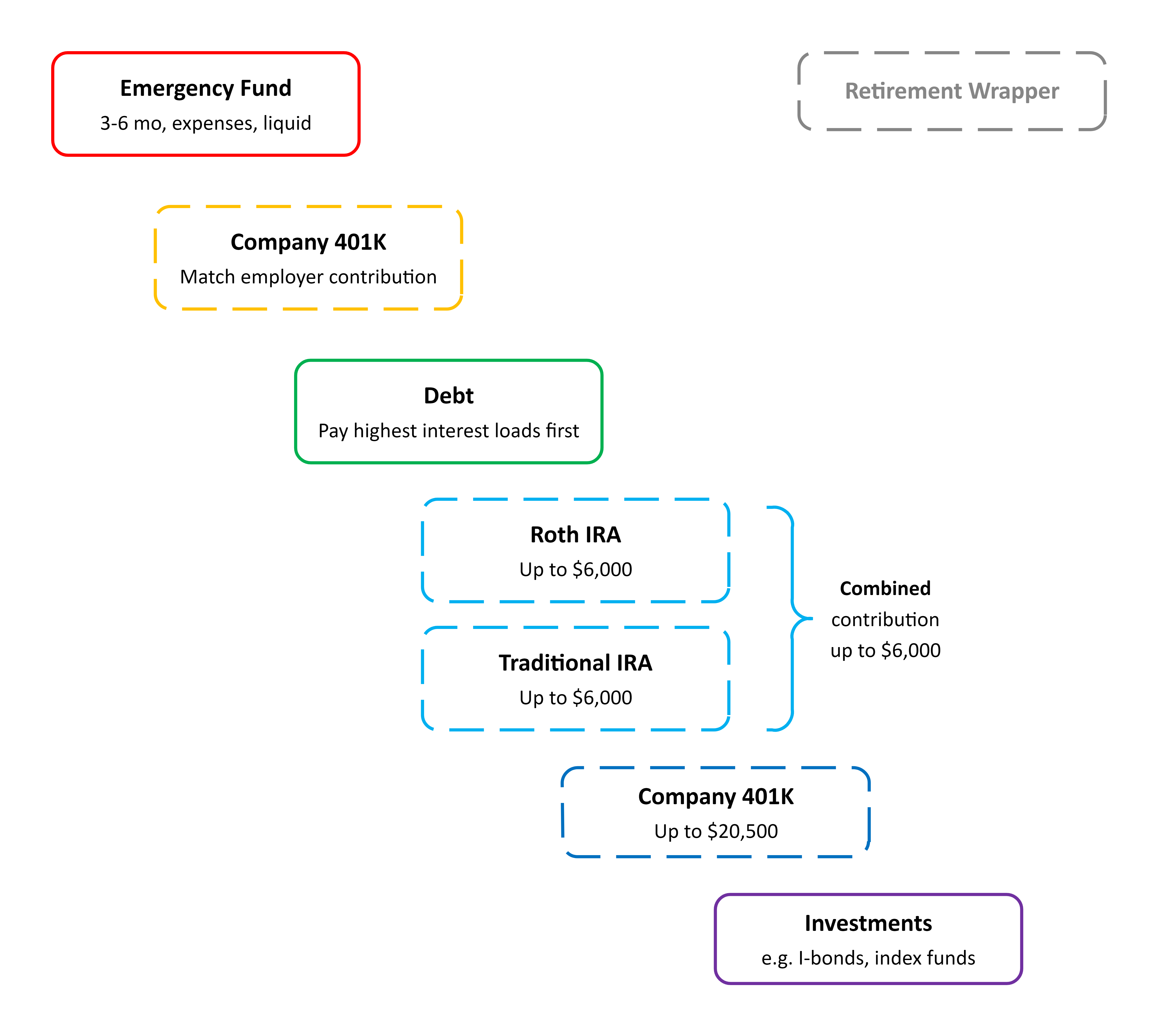

1. Establish an Emergency Fund

- Your first step should be creating a safety net for unexpected expenses, like medical emergencies or auto repairs.

- It is advised by financial professionals to set aside an amount equal to three to six months of living expenses as a safety net. This creates a buffer and ensures you don’t rely on debt during tough times.

2. Maximize Employer Contributions (e.g., 401(k))

- If your employer offers a retirement savings plan with matching contributions, take full advantage.

- If your employer offers to match a percentage of your contributions, like 5% of your salary, be sure to contribute at least that amount. This effectively boosts your retirement savings without additional cost to you.

3. Pay Off Debts Strategically

- Focus on eliminating high-interest debts, such as credit card balances, using methods like the debt avalanche (tackling the highest interest rates first) or the debt snowball (starting with smaller balances to build momentum).

4. Expand Retirement Contributions

- Once your debts are under control, increase contributions to retirement accounts like IRAs or 401(k)s. Aim to max out these accounts if possible, ensuring a comfortable retirement.

5. Continue Diversified Investments

- Allocate funds to diversified investments, such as mutual funds, stocks, or ETFs. This helps grow your wealth over time and protects your portfolio against market volatility.

Why Is Personal Finance Important?

Personal finance is more than just managing money — it’s about securing your future and achieving peace of mind. Proper financial planning helps you:

- Build wealth steadily over time.

- Avoid financial stress during emergencies.

- Meet both short-term goals (like vacations) and long-term goals (like retirement).

In short, a solid financial plan empowers you to live life on your terms.

Key Areas of Personal Finance Represented in a Flowchart

Here are the key areas of personal finance that can be represented in a flowchart:

1. Budgeting

- A well-planned budget is key to achieving financial stability. It helps you monitor your income and expenses to ensure you’re spending within your limits..

- Methods such as the 50/30/20 rule, allocating 50% of your income to necessities, 30% to discretionary spending, and 20% to savings and debt—can make budgeting more manageable.

2. Saving

- Saving isn’t just about putting money aside; it’s about setting clear goals.

- Whether it’s creating an emergency fund or saving for a down payment, a flowchart helps prioritize and track savings goals.

3. Investing

- Investing focuses on growing your money.

- A flowchart can guide you through the steps, from starting with low-risk investments to diversifying into stocks or real estate.

4. Financial Protection

- Insurance is essential for securing your assets. Whether it’s health, life, or property insurance, including this in your flowchart ensures you’re covered for unexpected events.

5. Tax Planning

- Effective tax planning helps you minimize liabilities and take advantage of deductions or credits.

- A flowchart can include reminders for periodic tax reviews and strategic adjustments.

6. Debt Management

- Managing debt is crucial for financial health. Incorporate strategies like consolidation, refinancing, or paying more than the minimum to reduce debt quickly.

How to Structure Personal Finance Using a Flowchart

A well-structured personal finance flowchart follows a logical sequence. For example:

- Start with budgeting to understand cash inflow and outflow.

- Move on to saving for emergencies.

- Include debt repayment strategies next.

- Finish with investments for long-term growth.

Examples Of Flowchart Template

We recommend using tools like EdrawMax, which offers customizable flowchart templates. Here’s an example of how your flowchart might look:

Functional Decomposition Example

Personal finance flowchart

Explore More Templates: Personal finance Flowchart templates

Advantages of Using a Personal Finance Flowchart

There are several benefits of using a personal finance flowchart:

- Simplifies Complex Decisions: Visualizing financial steps makes decision-making straightforward and approachable.

- Tracks Progress: Helps monitor your financial journey and highlights completed steps.

- Encourages Responsibility: A clear roadmap motivates you to stick to your goals and avoid distractions.

- Enhances Clarity: Outlines priorities, making it easier to decide between saving, investing, or debt repayment.

- Adapts to Changes Easily: You can update the flowchart to reflect life changes, such as a salary increase or unexpected expenses.

- Builds Financial Confidence: Seeing your plan visually boosts understanding and promotes smarter financial choices.

Common Uses of a Personal Finance Flowchart

- Retirement Planning

- A flowchart can outline specific steps, such as contributing to 401(k)s and IRAs.

- Emergency Fund Creation

- Visualizing the savings process ensures you build a solid safety net.

- Debt Reduction Strategies

- Flowcharts help prioritize debt repayment strategies, such as the snowball or avalanche methods.

- Balancing Short-Term and Long-Term Goals

- Use a flowchart to allocate resources between immediate needs and future goals.

Digital Tools for Creating Personal Finance Flowcharts

A particular finance flowchart is a great way to cover your financial condition. It’s essential to continue investing indeed after reaching your financial pretensions. Edraw Max is a free diagramming tool that can be used rather than pen and paper or other traditional tools.

You may also use other tools like Lucidchartand Canvato make it easy to produce visually appealing flowcharts. They offer features like drag-and-drop templates and customization options, making them perfect for both beginners and experts.

You might also like reading: How to Set Up Personal Finance App Using FlutterFlow.

Conclusion

A personal finance flowchart is more than just a planning tool, it’s a pathway to financial independence. By organizing your financial goals and breaking them into manageable steps, you can take control of your future with confidence. Whether you’re planning for retirement or reducing debt, a flowchart is your financial compass.

Frequently Asked Questions (FAQs)

What’s a Personal Finance Flowchart?

A personal finance flowchart is a visual tool that organizes your financial goals and the steps needed to achieve them. It breaks down complex financial decisions, such as budgeting, saving, investing, and debt repayment, into easy-to-follow steps, helping you manage your money effectively.

What Are the Steps of Personal Finance?

The essential steps of personal finance generally include:

1. Establishing an emergency fund

2. Maximizing employer retirement contributions (e.g., 401(k))

3. Paying off high-interest debt

4. Increasing retirement contributions

5. Diversifying investments for long-term growth

How Do You Structure Personal Finance?

Personal finance should be structured in a logical sequence:

1. Start with budgeting to track income and expenses.

2. Build an emergency fund.

3. Focus on paying off high-interest debt.

4. Increase retirement savings.

5. Begin investing in diversified assets for long-term growth.

What Are the 7 Steps in Personal Finance?

The seven key steps in personal finance are:

1. Set financial goals

2. Create a budget

3. Build an emergency fund

4. Eliminate high-interest debt

5. Save for retirement

6. Invest for growth

7. Protect your assets (insurance and estate planning)

What Are the 5 Main Components of Personal Finance?

The five main components of personal finance are:

1. Budgeting – Tracking income and expenses

2. Saving – Building an emergency fund and saving for goals

3. Investing – Growing wealth through stocks, bonds, and real estate

4. Insurance – Protecting your assets and health

5. Debt Management – Managing and paying off debts

What Are the 4 Pillars of Personal Finance?

The four pillars of personal finance are:

1. Income – Earnings from work or investments

2. Saving – Setting aside money for future goals

3. Investing – Growing wealth through assets

4. Protection – Insurance and risk management

How Do You Structure Personal Finance?

Personal finance should be structured in a logical sequence:

1. Start with budgeting to track income and expenses.

2. Build an emergency fund.

3. Focus on paying off high-interest debt.

4. Increase retirement savings.

5. Begin investing in diversified assets for long-term growth.

What Is Step 4 in Financial Planning?

Step 4 in financial planning generally involves implementing the strategy. This is where you start executing your financial plan, such as contributing to savings, investing, or paying off debts, based on the goals you’ve set.

What Are the 4 R’s of Credit Analysis?

The 4 R’s of credit analysis are:

1. Risk: Assessing the likelihood of repayment

2. Repayment Capacity: Ability of the borrower to repay the loan

3. Revenue: Income generated to cover loan repayments

4. Reputation: The borrower’s credit history