Are you looking to know why indexed universal life insurance (IUL) is a bad investment?

I have been researching different insurance options available for the last 3 years, and I found Index life insurance to be widely recognized. Most people say it is a good investment opportunity, but here is the reality:

One of the key reasons why Indexed Universal Life (IUL) is often viewed as a poor investment choice is because the total returns of the S&P 500 have consistently outperformed IUL across various decades. In an attempt to make IUL appear more favorable when compared to the S&P 500, insurance agents selectively focus on and highlight the worst-performing decades in the history of the stock market.

Be seated, as in the whole of this informative article, we will explore different aspects and angles of IUL and we are going to expose the reality in front of you.

Before defining why IUL is a bad investment, let’s understand: What is Indexed Universal Life Insurance (IUL)? So,

What is Indexed Universal Life Insurance (IUL)?

Indexed Universal Life Insurance (IUL) is a type of life insurance policy that offers both a death benefit and the potential for cash value accumulation. It has gained popularity in recent years due to its promise of flexible premiums and the opportunity to participate in the market’s upside potential. However, despite these perceived benefits, there are several reasons why IUL may not be the best investment choice for everyone.

How Does Indexed Universal Life (IUL) Insurance Work?

Similar to universal life insurance, Indexed Universal Life (IUL) policies offer flexibility with adjustable premiums. You have the option to underpay or skip premiums, and you may even be able to tweak your death benefit. What sets IUL apart is how the cash value is invested.

When you choose an IUL policy, the insurance company guides you in picking an index for the cash value account segment and your death benefit. When you pay a premium, part of it covers the insurance cost based on the insured person’s life; any fees are taken care of, and the remaining amount is added to the cash value.

The total cash value grows with interest based on increases in an equity index, though it’s important to note that it’s not directly invested in the stock market. If you have an IUL policy, you typically have the option to borrow against the accumulated cash value. However, it’s crucial to repay these loans because, if not, they are subtracted from the death benefit.

Still, thinking why iul is bad investment? Keep reading and you will get it.

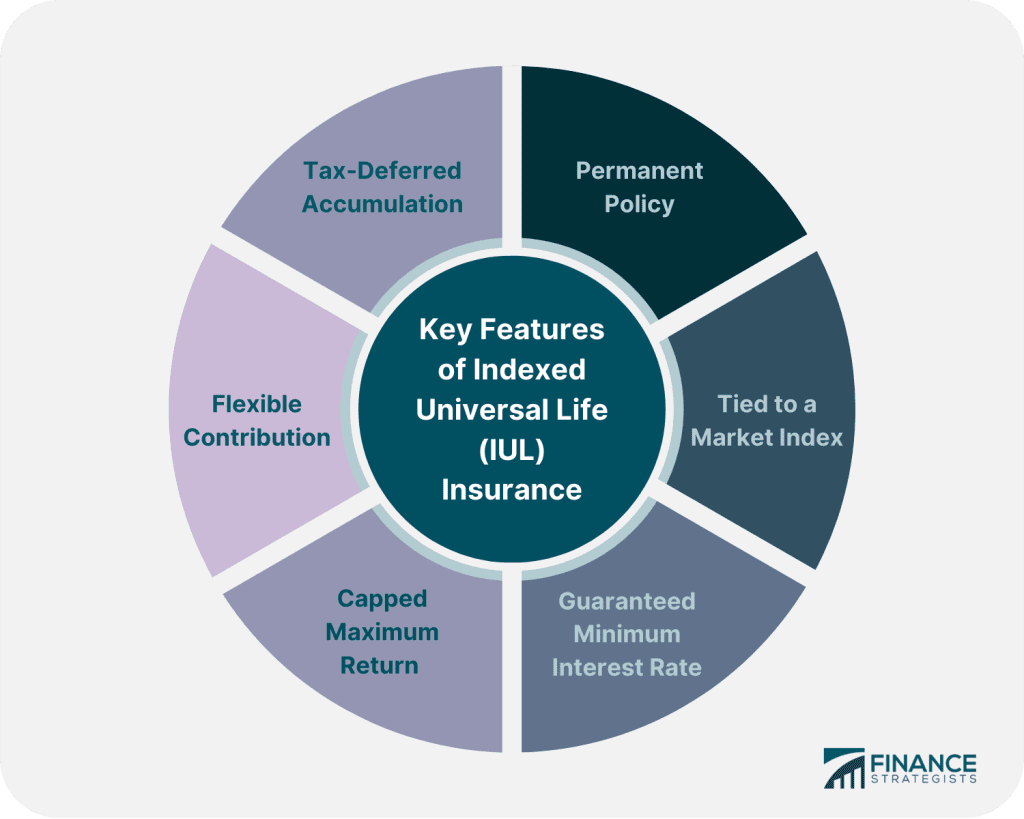

Key Features of IULs

Indexed Universal Life (IUL) insurance comes with several key features, including:

Advantages and Disadvantages of IUL Insurance: Why IUL is a bad investment?

Indexed Universal Life (IUL) insurance policies are not suitable for everyone, but they can be a good choice for those looking for permanent life insurance that comes with a cash component earning interest along with a death benefit. While these policies are generally pricier than term life insurance, they offer permanent coverage, and the death benefit is paid tax-free to your beneficiaries when you pass away. Additionally, the policy may grow in value over time because of the cash component, and in some cases, you might have the option to borrow from your account.

Now, let’s dive into the advantages and disadvantages of IUL which will then determine why iul is bad investment?

Advantages:

Disadvantages:

Furthermore, IUL policies are complex products that require careful monitoring and understanding. The intricacies of the policy structure, including fees, expenses, and the indexing method, can be overwhelming for the average investor. Without proper knowledge and guidance, it is easy to make costly mistakes that could negatively impact the policy’s performance. Now you can decide whether you should invest or not. We have considered a lot of things while diving into why IUL is a bad investment.

Example of Indexed Universal Life Insurance

Imagine you have an Indexed Universal Life Insurance (IUL) policy with a chosen index. Let’s say that the index gained 6% from the beginning to the end of June. Now, what happens is that this 6% is applied to your policy’s cash value. How this gain is calculated can vary; some policies sum up the changes over the period, while others average the daily gains for a month. Importantly, if the index goes down instead of up, no interest is credited to your cash account.

The gains from this index are added to your policy based on something called the “participation rate,” which is a percentage set by the insurance company. This rate can range from 25% to more than 100%. For instance, if the gain is 6%, the participation rate is 50%, and your current cash value is $10,000, you’d see $300 added to your cash value (6% x 50% x $10,000 = $300).

This process might sound good in theory, but keep in mind that these rates and calculations are determined by the insurance company, and they have a significant impact on how much your cash value grows.

{Read more: How to Make Money with Chat GPT Reddit: A Complete Guide }

Comparing IUL with Other Investment Options

When evaluating the suitability of IUL as an investment, it is crucial to compare it with other available options. Traditional investment vehicles, such as mutual funds or exchange-traded funds (ETFs), offer greater transparency, lower fees, and more control over investment decisions. Unlike IUL, these investment options do not come with surrender charges, allowing investors to access their funds when needed.

Additionally, investing in a diversified portfolio of stocks and bonds can provide better long-term returns compared to IUL. By spreading the risk across various asset classes, investors can mitigate market volatility and potentially achieve higher growth over time.

It is essential to consider your investment goals, risk tolerance, and time horizon when comparing IUL with other investment options. Seeking advice from a qualified financial advisor can help you make an informed decision based on your unique circumstances.

{Read more: AI Business Ideas you should never skip }

Examining the Performance of IUL Policies

To assess the performance of IUL policies, it is necessary to delve into historical data and real-world examples. While some IUL policies may have performed well during certain periods of market growth, it is crucial to consider the long-term track record. In many cases, the returns generated by IUL policies may not match the expectations set by insurance agents or the market indices they are linked to.

Moreover, the fees associated with IUL policies can significantly impact the overall performance. The costs of insurance, administrative fees, and other charges can eat into the potential investment gains, making it harder to achieve satisfactory returns.

It is vital to analyze the performance of IUL policies with a critical eye and consider the impact of fees on the overall returns. By doing so, you can gain a better understanding of whether IUL is a suitable investment choice for your financial goals.

The Role of Lincoln Investment in the IUL Market

Lincoln Investment is a prominent player in the IUL market, offering a range of indexed universal life insurance policies. While Lincoln Investment and other insurance companies provide IUL policies as a means of accumulating cash value and protecting loved ones, it is essential to carefully evaluate the terms and conditions of these policies.

As mentioned earlier, IUL policies often come with high fees and complex structures that can erode potential investment gains. It is crucial to thoroughly review the policy terms, including participation rates, caps, and floors, to fully understand the potential limitations and risks associated with the policy.

Seeking independent investment advice can help you navigate the complexities of IUL policies and make an informed decision that aligns with your financial goals.

{Read more: 5 Tips on Investment for Beginners you must know }

The Importance of Independent Investment Advice

When considering an investment option as complex as IUL, independent investment advice plays a vital role. Independent financial advisors are not tied to any specific insurance company or investment product, allowing them to provide unbiased guidance tailored to your individual needs.

An independent financial advisor can assess your financial situation, goals, and risk tolerance to determine whether IUL or alternative investment options are suitable for you. They can also help you understand the intricacies of IUL policies, including the potential drawbacks and limitations, and guide you toward making an informed decision.

Rather than relying solely on the recommendations of insurance agents or sales representatives, seeking independent investment advice can provide you with a broader perspective and help you make the best choice for your financial future.

Using an Investment Calculator to Evaluate IUL

To evaluate the potential returns and drawbacks of an IUL policy, it can be helpful to use an Investment calculator that allows you to input various parameters, such as premium amounts, policy terms, and expected market returns, to estimate the potential cash value accumulation and death benefit of an IUL policy.

By using an investment calculator, you can compare the projected returns of an IUL policy with alternative investment options. This can provide valuable insights into the long-term implications of choosing IUL as an investment vehicle and help you make a more informed decision.

Alternative Investment Strategies to Consider

While IUL may not be the best investment choice for everyone, there are alternative strategies worth exploring. Traditional investment options, such as mutual funds, ETFs, or individual stocks and bonds, offer greater flexibility, transparency, and control over investment decisions.

Diversifying your investment portfolio across different asset classes, such as equities, fixed income, and real estate, can help mitigate risks and potentially achieve higher long-term returns. Working with a qualified financial advisor can help you determine the optimal asset allocation based on your risk profile and investment goals.

Additionally, exploring other insurance products, such as term life insurance or disability insurance, can provide essential protection while freeing up funds to invest in more suitable investment options.

Conclusion: Making an Informed Decision about IUL

Indexed Universal Life Insurance (IUL) may seem like an attractive investment option due to its potential for cash value accumulation and tax advantages. However, it is crucial to carefully evaluate the drawbacks and limitations of IUL policies before making a decision.

Factors such as high surrender charges, potential underperformance, complex structures, and lack of liquidity can make IUL a less desirable investment choice compared to other alternatives. By comparing IUL with traditional investment options and seeking independent investment advice, you can make a more informed decision that aligns with your financial goals and risk tolerance.

Investing in a diversified portfolio of assets, guided by a qualified financial advisor, can provide you with greater control, transparency, and potentially higher long-term returns compared to IUL.

Frequently asked questions

Can you lose money in an IUL?

Yes, there is a potential for loss, as IUL returns are tied to market performance. However, most policies have a floor that prevents a negative cash value.

What is a drawback to IUL?

Drawbacks include potential complexity, caps on returns, and the impact of market downturns on cash value growth.

What is better than an IUL?

The best choice depends on individual financial goals. There are certain better options such as mutual funds, ETFs, or individual stocks and bonds available in the market.

What are the disadvantages of universal life insurance?

Disadvantages include complexity, potentially high costs, and the impact of market fluctuations on cash value growth.

How much money can I put in an IUL?

The amount varies but generally has a maximum determined by the insurance company and IRS regulations. It’s crucial to stay within IRS guidelines for tax benefits.

Is an IUL a good product?

It can be beneficial for those seeking life insurance with potential cash value growth tied to market performance. However, it’s essential to understand its features and limitations.

Is an IUL expensive?

IUL premiums can be higher than term life insurance. The costs depend on factors like coverage amount, age, health, and policy features.

How does money grow in an IUL?

The cash value in an IUL grows through credited interest linked to a market index. Some policies may have caps or participation rates limiting the growth.

Is an IUL permanent?

Yes, an IUL is a form of permanent life insurance, providing coverage for the entire lifetime of the insured as long as premiums are paid.

Want to Read more:

TornadoCash: Your shield against surveillance on the blockchain. Explore the power of privacy with decentralized transactions

“Thank you for highlighting TornadoCash! It’s indeed a powerful tool for enhancing privacy in decentralized transactions. Delving into the world of blockchain privacy can be eye-opening. Let me know if you have any questions or need further information!”